Tax Deduction

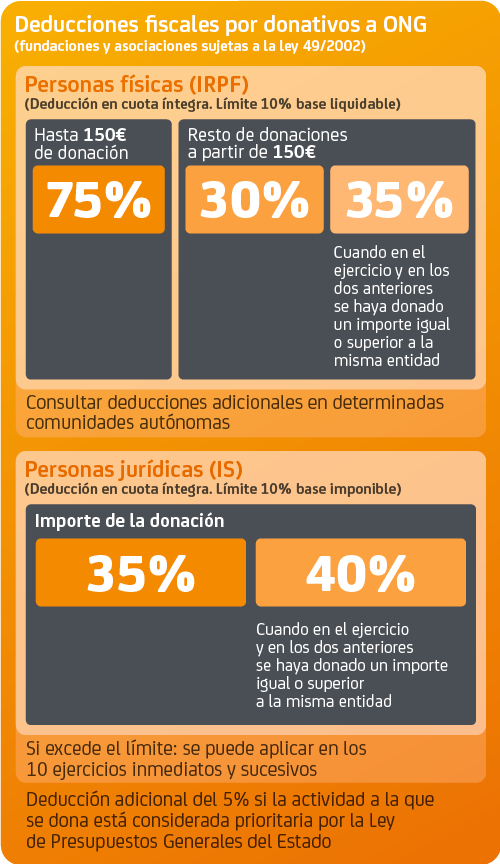

There are deductions for donations to NGOs, both in Personal Income Tax (IRPF) and in Corporate Income Tax (IS). For this, the donor (individual or institution) must have the tax certificate of the NGO. The amount of the deduction varies according to the tax regime to which the organization with which you have collaborated is subject.

In addition, you must take into account if your autonomous community is subject to a particular charter or if you have additional deductions. If the activity in which you have collaborated has been classified as a priority patronage activity by Law 49/2002, you may be entitled to a higher percentage of deduction.

Deductions in Personal Income Tax:

• Foundations and associations subject to law 49/2002 (entities qualified by law in its article 16 and provisions 5, 6, 7, 9 and 10 and consortia referred to in its article 27.2 second): deduction of 75% for The first 150 euros donated. From this amount, donations will be deductible at 30% or 35% if they are periodic donations made for at least three years to the same entity for an amount equal to or greater. The deduction has a limit of 10% of the base taxable of the tax.

• Foundations and associations declared of Public Utility not subject to law 49/2002 (article 69.3 RD Legislative 3/2004 of the consolidated text of the Personal Income Tax Law): deduction of 10% of the amount of the donation with a limit of 10% Of the taxable base, in the case of foundations.

• Undeclared associations of Public Utility: there are no deductions for the donations to these entities.

Deductions in Corporate Tax:

Donations to NGOs are not deductible expenses in Corporate Income Tax. However, they may give rise to tax deductions in installments to the extent that the entity receiving the grant (foundation or association of public utility) can and has opted for the special tax regime of Law 49/2002 on taxation of Non-profit organizations and tax incentives for patronage.

The percentage of tax deduction in Corporate Income Tax is 35% (with the limit of 10% of the tax base). This deduction is increased to 40% for donations made to the same entity for the same or higher amount for at least three years. Amounts not deducted can be applied for tax periods ending in the next 10 years.